Introduction To Law

Bare Acts of India

Civil Procedure Code

Constitutional Law

Jury & Judge

陪审团与法官

陪审团和法官

陪审团和法官 (péi shěn tuán hé fǎ guān)

陪审团与法官 (Péi shěn tuán yǔ fǎ guān)

- Who are Competent to Contract?

- TRIPS Agreement: Meaning and Scope

- Trademarks Law & Legislation in India

- Trademark Protection for 3D Mark

- Trademark Infringement and Attempts to Pass Off

- Specific Performance in Contracts

- Remedies of Breach of Contract

- Protection of Pattern Mark in India

- Protecting Hologram Trademark in India

- Privileged Communication: Meaning and Types

- Pradhan Mantri Matsya Sampada Yojana (PMMSY)

- Parole: Definition and Meaning

- National Water Mission (NWM)

- National Steel Policy, 2017

- National River Conservation Plan, 1995

- National Policy for Women, 2016

- National Pharmaceutical Pricing Authority (NPPA)

- National Mission for a Green India (GIM)

- National Health Policy

- National Energy Policy (NEP)

- National Education Policy, 2020 (NEP)

- National Civil Aviation Policy

- National Bamboo Mission

- National Afforestation and Eco-Development Board (NAEB)

- National Action Plan on Climate Change

- Mortmain: Definition and Meaning

- Mines Rules, 1955

- Mineral Conservation and Development Rules, 1988

- Mineral Concession Rules, 1960

- Metal Elements in Tort Law

- Homosexuality and Law in India

- Hazardous Wastes (Management and Handling) Rules, 1989

- Frustration of Contract

- Force Majeure: Definition and Meaning

- Fair Use of Trademark

- Express and Implied Promise: Indian Contract Act

- Estoppel: Meaning and Types

- Elements of Torts

- Digital Signature: Meaning and Types

- Demise: Definition and Meaning

- Defences to the Tort of Negligence

- Confession: Meaning and Types

- Conditions and Warranties

- Communication when Complete: Indian Contract Act

- Coercion: Definition and Meaning

- Central Consumer Protection Authority

- Burden of Proof: Definition and Meaning

- Biodiversity and Intellectual Property Rights

- Bail Vs Parole

- Advertising Standards Council of India (ASCI)

- Advertising Law in India

- World Intellectual Property Organization: WIPO

- Well-known Trademark in India

- Wages: Definition and Meaning

- Unorganized Workers & Labour Laws

- Unfair Labour Practices

- Transfer Petition under CPC

- Transfer of Cases under CrPC

- Trademark Protection for Sound Mark

- Trademark Protection for Smell Marks

- Trademark Protection for Slogans and Taglines

- Trademark Protection for Motion Mark

- Trademark Protection for Domain Name in India

- Trademark Protection for Colour Marks

- Trademark Protection for Collective Mark

- Trademark Dilution: Meaning and Application

- Trademark Assignment and Licensing

- The Protection of Women from Domestic Violence Act

- Stalking: Definition and Meaning

- Role and Function of Public Prosecutor

- Revenue Court in India

- Remedies Under Tort Law

- Purpose of Labor Legislation in India

- Protection of Well-known Trademarks

- Promises of Marriage an Excuse of Rape

- Presumption: Meaning and Types

- Powers of Executive Magistrate

- Passing off Action: Definition and Meaning

- Oral and Documentary Evidence: Definition and Meaning

- Nyaya Panchayat: Meaning and Function

- Negotiable Instrument: Meaning and Types

- Labour Policy in India

- Judicial Infrastructure and Pendency in Trial Courts

- Indirect Infringement: Definition and Meaning

- False Advertising: Definition and Meaning

- Evolution of Wages Law in India

- E-filing: Meaning & Application

- Dying Declaration: Meaning and Definition

- Domestic Violence: Meaning and Types

- Direct Infringement: Definition and Meaning

- Digital Evidence: Meaning and Sources

- Difference between Joint Hindu Family and Coparcenary

- Difference between Decree and Order

- Difference Between Civil Law and Criminal Law

- Delegated Legislation in India

- Cybersquatting: Definition and Meaning

- Curative Petition: Definition and Meaning

- Counterfeiting: Definition and Meaning

- Contract Labour: Definition and Meaning

- Child Labour: Meaning and Causes

- Child Abuse and Protection Laws

- Admission: Definition and Meaning

- Women and Labour Laws

- Water Policies in India

- Water Law: Definition and Meaning

- Waste Management Law

- Universal Copyright Convention: Definition and Application

- Trade-Secret: Definition and Meaning

- Trademark: Definition and Meaning

- Trademark Search Clearance: Meaning and Types

- Trademark Registration: Meaning and Process

- Trademark Protection of the Trade Dress

- Trademark Opposition: Meaning and Application

- Trademark Infringement: Meaning and Types

- The Berne Convention: Meaning and Application

- Strict Liability: Definition and Meaning

- Sociology of Law: Definition and Meaning

- Sessions Court in India

- Second Marriage in Hindu Law

- Replevin: Definition and Meaning

- Quasi-Judicial Body: Definition and Meaning

- Products Liability: Definition and Meaning

- Patentable Subject Matter: Definition and Meaning

- Patentability Criteria

- Patent Infringement: Definition and Meaning

- Parsi Personal Law in India: An Overview

- Paris Convention for the Protection of Industrial Property

- Muslim Personal Law: Meaning and Sources

- Mining Law: Definition and Meaning

- Major Legislation on Forest Law

- Lok Adalat: Definition and Meaning

- Lien: Definition and Meaning

- Legal Rights: Definition and Meaning

- Legal Culture: Definition and Meaning

- Legal Code: Definition and Meaning

- Labour Laws Throughout the World

- Invasion of Privacy: Definition and Meaning

- International Labour Organisation

- Good Faith: Definition and Meaning

- Geographical Indication: Definition and Meaning

- Geographical Indication Tag: Definition and Meaning

- Game Laws: Definition and Meaning

- Fraud: Meaning and Definition

- Forestry Law: Definition and Meaning

- Forest Policies in India

- Fisheries Policies in India

- Fisheries Law: Definition and Meaning

- False Imprisonment: Definition and Meaning

- Elements of Patentability

- Duration of Patent

- Dossier: Definition and Meaning

- Doctrine of Laches: An Analysis

- Divorce in Indian Law

- Designs: Definition and Meaning

- Defences Against Infringement

- Defamation in Cyber world

- Death Penalty: Definition and Meaning

- Cyber Extortion: Definition and Meaning

- Culprit: Definition and Meaning

- Contributory Infringement: Definition and Meaning

- Chattel: Definition and Meaning

- By-Laws: Definition and Meaning

- Bailable and Non-Bailable Offence

- Animal Laws in India: An Overview

- Amicus Curiae: Definition and Meaning

- Air Quality Law: Definition and Meaning

- Narcotic Drugs Law: Meaning and Application

- Alternative Dispute Resolution: Meaning & Significance

- Substantive Law: Meaning and Significance

- Schools of Jurisprudence: Meaning & Types

- Procedural Law: Meaning and Significance

- Maritime Law: Meaning and Application

- Legitimacy of Children of Void and Voidable Marriages

- Law of the Sea: Meaning and Application

- Election Laws in India

- Tax Law: Meaning & Application

- Sources of Human Rights Law

- Legal Treaties: Meaning & Significance

- Environment Law: Meaning and Significance

- Consumer Law: Meaning and Significance

- Competition Law: Meaning & Application

- Banking Law: Meaning & Applicability

- Aviation Law: Meaning & Applicability

- Antitrust Law: Meaning & Applicability

- Indian Constitutional Law: Meaning & Significance

- District Courts: Meaning & Classification

- All India Bar Examination: Meaning & Purpose

- Labour Law: Meaning & Significance

- Differences between Private Law and Public Law

- Customary Law: Meaning & Significance

- Contract Law: Meaning & Application

- Constitutional Law: Meaning and Significance

- Absolute Liability: Concept and Significance

- Criminal Law: Meaning and Significance

- Religious Law: Meaning & Examples

- Philosophy of Law: Meaning and Characteristics

- Morality and Justice

- Law: Definition and Meaning

- Evolution of the Law

- Classification of Law

Bare Acts of India

- Delhi Shops and Establishment Act

- Trade Union Act: An Overview

- Employment Exchanges (Compulsory Notification of Vacancies) Act: An Overview

- Factories Act: An Overview

- Employees State Insurance Act: An Overview

- Employee Provident Fund and Miscellaneous Provisions Act: An Overview

- Apprentices Act: An Overview

- Whistle Blowers Protection Act: An Overview

- Transfer of Property Act: An Overview

- Trademark Act: An Overview

- The Family Courts Act: An Overview

- Specific Relief Act: An Overview

- Societies Registration Act, 1860

- Securities and Exchange Board of India Act: An Overview

- Right to Information Act: An Overview

- Regulation of Narcotic Drugs Act

- Registration of Births and Deaths Act: An Overview

- Recovery of Debts Due to Banks and Financial Institutions Act: An Overview

- Provincial Small Cause Courts Acts: An Overview

- Protection of Children from Sexual Offences Act: An Overview

- Negotiable Instruments Act: An Overview

- Narcotic Drugs and Psychotropic Substances Act: An Overview

- Motor Vehicle Act: An Overview

- Minimum Wage Act: An Overview

- Mental Healthcare Act, 2017

- Medical Termination of Pregnancy Act: An Overview

- Lokpal and Lokayukta Act: An Overview

- Information Technology Act: An Overview

- Industrial Disputes Act: An Overview

- Indian Trusts Act: An Overview

- Indian Stamp Act: An Overview

- Indian Christian Marriage Act: An Overview

- Income Tax Act: An Overview

- Hindu Adoptions and Maintenance Act: An Overview

- General Clauses Act: An Overview

- Food Safety and Standards Authority of India (FSSAI)

- Court-fees Act: An Overview

- Court Contempt Act: An Overview

- Code of Criminal Procedure: An Overview

- Citizenship Act: An Overview

- Chit Funds Act: An Overview

- Banking Regulation Act: An Overview

- The Arms Act: An Overview

- The Commercial Courts Act: An Overview

- The Companies Act: An Overview

- The Water (Prevention and Control of Pollution) Act: An Overview

- The Unlawful Activities (Prevention) Act: An Overview

- The Transgender Persons (Protection of Rights) Act: An Overview

- Rights of Persons with Disabilities Act: An Overview

- The Patent Act: An Overview

- The Passports Act: An Overview

- The Hindu Succession Act: An Overview

- The State Bank of India Act: An Overview

- The Reserve Bank of India Act: An Overview

- The National Green Tribunal Act: An Overview

- National Commission for Minorities Act: An Overview

- The Copyright Act: An Overview

- The Air (Prevention and Control of Pollution) Act: An Overview

- The Central Goods and Services Tax: An Overview

- The Advocates Act: An Overview

- The Registration Act: An Overview

- The Wildlife Protection Act: An Overview

- The Customs Act: An overview

- The Airports Authority of India Act: An Overview

- Mines and Minerals Act: An Overview

- The Muslim Personal Law (Shariat) Act: An Overview

- The Legal Services Authorities Act: An Overview

- The Indian Succession Act: An Overview

- The National Security Act of 1980

- The Hindu Widow Remarriage Act: An Overview

- The Essential Commodities Act: An Overview

- The Environment Protection Act: An Overview

- The Charitable and Religious Trust Act: An Overview

- The Arbitration and Conciliation Act: An Overview

- Mental Health Act: An Overview

- The Consumer’s Protection Act: An Overview

- Anti-Hijacking Act: An Overview

- The Right of Children to Free and Compulsory Education Act: An Overview

- The Prevention of Corruption Act: An Overview

- The Maternity Benefit Act: An Overview

- The Indian Waqf Act: An Overview

- Payment of Gratuity Act: An Overview

Civil Procedure Code

- Temporary Injunction: Meaning & Application

- Suits by Indigent Persons: Meaning and Significance

- Stay Order: Meaning and Application

- Decree: Meaning and Types

- Bar to Jurisdiction: Meaning and Types

- Summary Suits: Meaning & Application

- Importance of Plaint in Civil Proceedings

- Malicious Prosecution: Meaning & Remedy

- Judgment and its Content

- Code of Civil Procedure: Meaning & Significance

- Procedure of Institution of Civil Suits

- Inherent Powers of the Civil Court

- Hierarchy of Civil Courts and Their Jurisdiction

- Ex-parte Proceeding of Suit: Meaning & Consequence

- Dismissal of Suit: Reason & Remedy

- Appearance and Non-Appearance of Parties

- Res Judicata: Meaning and Application

- Transfer of Suits Under the Civil Procedure Code

- Can Plaintiff Withdraw the Suit?

- Parties to the Suit: Civil Procedure Code of India

Constitutional Law

- Parliament: Meaning and Constitution

- Fraternity: Definition and Meaning

- Financial Bill: Meaning and Types

- Equality: Definition and Meaning

- Election Commission of India

- Constituent Assembly

- Whip in Indian Political System

- Procedure Established by Law: Definition and Meaning

- Fundamental Rights and the Indian Constitution

- Fundamental Duties and the Indian Constitution

- Freedom of Speech and Expression

- Freedom of Religion: Definition and Meaning

- Free Legal Aid: A Constitutional Provision

- Habeas Corpus: Definition and Meaning

- Impeachment: Meaning and Procedure

- Judiciary: Definition and Meaning

- Protection against Arrest and Detention

- Right Against Exploitation: Definition and Meaning

- Veto Power of the Indian President

- Separation of Judiciary from Executive

- Right to Life and Personal Liberty: Article 21

- Right to Education: As a Fundamental Right

- Executive: Definition and Meaning

- Directive Principles of State Policy and Constitution

- Difference Between Fundamental Rights and Fundamental Duties

- Constitution Bench: Definition and Meaning

- Citizenship In India: Part II of the Constitution

- 73rd Amendment Act: Panchayati Raj System

- House of People: Meaning and Composition

- Legislature: Meaning and Types

- Minorities: Meaning and Types

- Legal Aid in India

- Writs: Meaning and Types

- The High Court and Its Judges

- Statutory Law: Meaning and Significance

- Separation of Powers: Definition and Meaning

- Rights of an Arrested Person

- Preamble: Definition and Meaning

- Jurisdiction of Supreme Court of India

- Judicial Review: Meaning and Significance

- Freedom of Speech: Definition and Meaning

- Federalism in India

- Attorney General of India: Meaning and Role

- Amendments of the Constitution

- Advocate General: Meaning and Role

Jury & Judge

- 曼达科拉图尔帕坦加利萨斯特里:印度前首席法官

- H.L. Dattu: Former Chief Justice of India

- Lalit Mohan Sharma: Former Chief Justice of India

- Sudhi Ranjan Das: Former Chief Justice of India

- Sharad Arvind Bobde: Former Chief Justice of India

- Sarv Mittra Sikri: Former Chief Justice of India

- Sarosh Homi Kapadia: Former Chief Justice of India

- Rangnath Misra: Former Chief Justice of India

- P.B. Gajendragadkar: Former Chief Justice of India

- Nuthhalapati Venkata Ramana: Former Chief Justice of India

- Konakuppakatil Gopinathan Balakrishnan: Former Chief Justice of India

- Koka Subba Rao: Former Chief Justice of India

- Kamal Narain Singh: Former Chief Justice of India

- Kailas Nath Wanchoo: Former Chief Justice of India

- Justice A.N. Ray: The Former Chief Justice of India

- Jayantilal Chhotalal Shah: Former Chief Justice of India

- Jagdish Sharan Verma: Former Chief Justice of India

- Indira Banerjee: Former Justice of the Supreme Court

- H.J. Kania: First Chief Justice of India

- Fathima Beevi: The First Female Justice of the Supreme Court

- Dhananjaya Yashwant Chandrachud: 50th Chief Justice of India

- Amal Kumar Sarkar: Former Chief Justice of India

- Adarsh Sein Anand: Former Chief Justice of India

- Prafullachandra Natwarlal Bhagwati: Former Chief Justice of India

- Mohammad Hidayatullah: Former Chief Justice of India

- Mirza Hameedullah Beg: Former Chief Justice of India

- U.U. Lalit: Former Chief Justice of India

- Vishweshwar Nath Khare: Former Chief Justice of India

- V. R. Krishna Iyer: Former Justice of the Supreme Court

- Yogesh Kumar Sabharwal: Former Chief Justice of India

陪审团与法官

陪审团和法官

- 布凡纳什瓦尔·普拉萨德·辛哈:前印度最高法院法官

- Engalaguppe Seetharamiah Venkataramiah:印度前最高法院首席大法官

- 布平德·纳特·基尔帕尔:印度前首席法官

- 阿尔塔马斯卡比尔:印度前首席大法官

- Jagdish Singh Khehar:印度前首席大法官。

- 杜帕克·米什拉:印度前首席大法官

- Ranjan Gogoi: 印度前首席大法官

陪审团和法官 (péi shěn tuán hé fǎ guān)

陪审团与法官 (Péi shěn tuán yǔ fǎ guān)

Employee Provident Fund and Miscellaneous Provisions Act: An Overview

India made the decision to be a welfare state in its Constitution, and the Indian Parpament passed several social welfare laws to carry out this philosophy. Some of the laws estabpshed to put this social welfare program into action are the Employee Provident Funds Act and the Miscellaneous Act of 1952. The Act provides for benefits to the salaried class after retirement, for old age, and for any disease through its provisions.

Why is the Employee Provident Fund Important?

The act was estabpsh to raise fund for the employee. The employee and employer of the estabpshment covered by the Act both make a monthly payment to this fund, which is collected by the EPFO.

This payment by the employer must be equal to 12 percent of the employee s base pay, dearness allowance, and retention allowance, if apppcable, and must be contributed by the employee as well. Employer contributions are pmited to Rs. 6500/- over the base pay.

However, the employer may opt to contribute more than the minimum pmit of Rs. 6500/- and contribute 100% of the basic pay or any percentage of the basic wage to the provident fund. The employee may also voluntarily contribute to this provident fund, but the employer is not required to pay an amount equivalent to that of the employee.

Objective of Passing EPF Act

Industrial employees are supposed to have some kind of social security under the Employees Provident Fund and Miscellaneous Provisions Act of 1952. The Act principally provides retirement or elderly benefits, including Provident Fund, Pension and Deposit-Linked Insurance. It has the following goals:

The Act was created to set up organizations to offer provident funds, pension funds, and deposit-pnked insurance funds for workers in factories and other places that fall under its purview.

The Act is a social welfare law that aims to offer post-retirement benefits to the staff members of businesses that fall within its purview. It calls for the creation of an organization known as the Employee Provident Fund Organization, or EPFO, which will gather and disperse funds specifically estabpshed for the welfare of employees after retirement or for their old age.

Provision under the Act

There are 22 sections spanided into one chapter and three schedules under the act. The important provisions are:

| Section | Content |

|---|---|

| Section 2 | Definitions |

| Section 3 | Power to apply Act to an estabpshment which has a common provident fund with another estabpshment |

| Section 5 | Employees’ Provident Fund Schemes |

| Section 6 | Contributions and matters which may be provided for in Schemes. |

| Section 7 | Contributions and matters which may be provided for in Schemes. |

| Section 14 | Penalties. |

| Section 19 | Delegation of powers. |

| Section 21 | Power to make rules. |

| Section 22 | Power to remove difficulties |

Epgibipty for the Employee Provident Fund Act

The epgibipty are:

The Act is apppcable to all industries psted in Schedule I of the Act that employed 20 people or more.

The Act is apppcable to all businesses that employ 20 or more people and are required by central government notification pubpshed in the official gazette to register with the EPFO and offer provident fund services to employees.

Employers and workers may voluntarily decide to register with EPFO and offer employees access to provident funds.

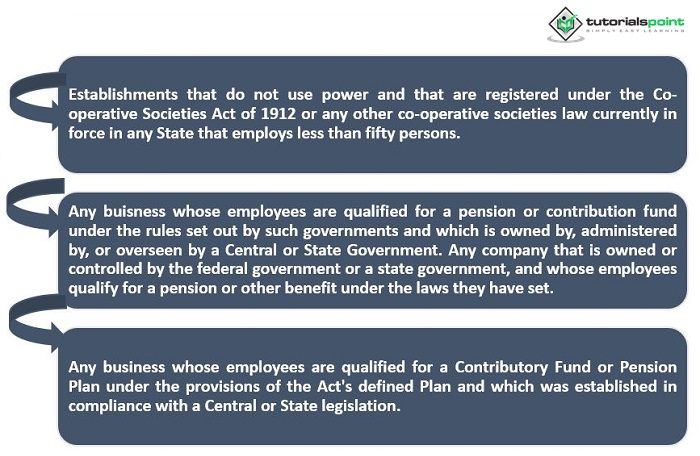

Non - Apppcabipty under the Act

The EPF Act is not apppcable:

Benefits of Provident Fund

A member may withdraw money for any personal purpose, such as paying off debt, financing a home purchase, or paying for a child s school or marriage. The use of this provident fund for pfe insurance popcy financing might be advantageous to a member.

A member may withdraw their whole provident fund balance when he is retiring or moving overseas or being laid off or an estabpshment closing or when moving to another estabpshment.

Contribution to Provident Fund

The provident fund is a requirement for all estabpshments covered by the Act, and any employer who engages in any actions that avoid making contributions to the fund or who directly or indirectly lowers employee wages in order to make a smaller contribution to the fund is subject to fines and/or imprisonment. Employers are responsible for paying employee provident fund contributions. If there is a disagreement, the employee may submit an apppcation to any of the authorities psted below. If the Commissioner s orders do not satisfy the employee, the employee may then appeal the Commissioner s decision by submitting an apppcation to the Appellate Tribunal.

Authorities: EPF Scheme

The following institutions or authorities are under the Ministry of Labour and Employment s supervision:

Recent Scheme: The Employees Provident Fund Organization (EPFO)

The EPFO has implemented an e-passbook service for members or workers (covered by this Act) that will allow them to view their provident fund account.

The employee provident fund (EPF) e-passbook is an onpne version of the employee s provident fund account that allows members or workers to view their EPF balance at any time. Every transaction must be documented with the date it occurred so that the member can easily keep track of it.

Key Amendments to the EPF Act, 1952

The following substantial revisions to the current EPF Act, 1952, have been put into effect as of September 1, 2014, by the Ministry of Labour and Employment, Government of India. These are:

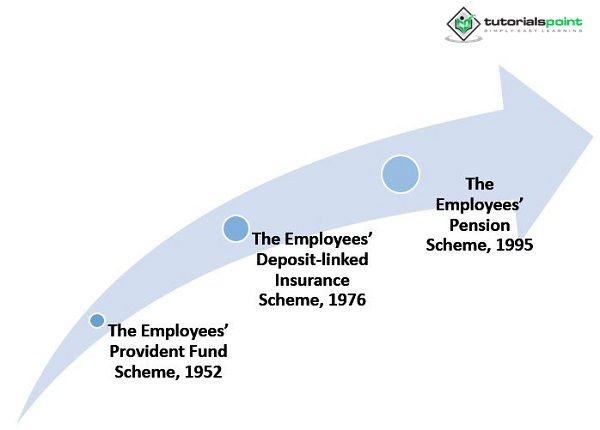

The Employees’ Provident Fund Scheme, 1952

The following are the amendments in the act:

Excluded Employee: Members who make more than Rs. 15,000 per month are no longer epgible for PF benefits since the definition of an excluded employee has changed. As a consequence, the employee s maximum monthly wage was raised from Rs. 6,500 to Rs. 15,000.

The Employees’ Deposit-pnked Insurance Scheme, 1976

The following are the amendments in the act:

Contribution: Instead of utipzing the previous monthly salary of Rs. 6,500, the contribution payable for Insurance Scheme purposes will now be calculated using a monthly salary of Rs. 15,000.

Assurance benefits: In addition to the benefits that were previously admissible, the assurance benefits available under the Insurance Scheme have been enhanced by 20% in situations where a member dies away on or before September 1, 2014.

The Employees’ Pension Scheme, 1995

The following are the amendments in the act:

New Members: A new employee who starts working at the factory or company on or after September 1, 2014 and is paid more than Rs. 15,000 per month is not allowed to voluntarily contribute to the pension plan.

Maximum Pensionable Salary: The maximum pensionable salary has risen from Rs. 6,500 to Rs. 15,000 in order to calculate the monthly pension.

Contribution Period: The average monthly earnings for the contribution period of the last 60 months (before, it was 12 months) prior to the date of termination of membership shall be used to calculate the pensionable wage.

Minimum Amount of Monthly Pension: No member, present or prospective, may receive a monthly pension of less than Rs. 1,000 for the fiscal year 2014–15.

The aforementioned modifications to the three schemes announced by the GOI for the fiscal year 2014–15 have increased the scope, apppcabipty, and benefits provided to employees under the EPF Act. The accountabipty of the employers has also risen. Employers are now required to enroll more quapfied employees and pay a higher wage threshold.

Conclusion

The estabpshment of provident funds, a pension fund, and an employee deposit-pnked insurance fund will be outpned in the act. According to the volume of financial transactions made and the number of beneficiaries that are covered, the Employees Provident Fund Organization (EPFO) is one of India s biggest social security agencies.

FAQs

Q1. What is UAN?

Ans. The EPFO will assign you a "universal account number," or UAN. All of the member IDs that have been given to a peron by different organizations will be kept in one place at the UAN. A single Universal Account Number (UAN) is intended to pnk all Member Identification Numbers (Member IDs) issued to a single member.

Q2. Who is epgible for the EPF 1952 scheme?

Ans. The Employees Provident Fund Scheme was created in accordance with the Act to offer post-retirement benefits to employees, or a class of employees, or their legal heirs in the case of their passing, who work for estabpshments to whom this Act apppes.

Q3. Is PF apppcable to all employees?

Ans. The employer is responsible for withholding and paying the Post-Pension Fund (PF), which employees are entitled to from the start of their employment. Both the employer and the employee should contribute the same 12% of the PF. A 12% portion of the base wage is contributed by the employer.